Setting out to purchase a new home isn’t like a trip to the store, where you grab your debit card and go to the store to select your purchases. There are some things to square away before you call a Realtor or go house hunting. Unless you’ve just won the lottery, one of the things which most home buyers must have is a mortgage. A mortgage is a loan that allows you to purchase a home and repay a lender over time based on an agreed upon set of conditions and specified interest rate.

Obtaining a mortgage is a process which requires planning. There is a phrase which originated with the military and is frequently used to describe what happens when one doesn't plan. Referred to as ‘The 6 P's,’ the phrase is, “Proper Prior Planning, Prevents Poor Performance.” Nowhere is this more true than when getting a new home mortgage. Step one in the process is a good credit score. Your credit ought to be in tip-top shape. Read our article on checking your credit score. And you must have your down payment in the bank as well.

With credit in order and down payment in savings, what comes next? Knowing how much home you can afford and what the approximate costs for a mortgage will be is the next step in the process.

Use a mortgage calculator to help plan

Should you want to know what your potential payments are based on the amount you might borrow, head on over to our online mortgage calculator section. In only a few short steps, you can receive an approximation of the monthly payment for your home.

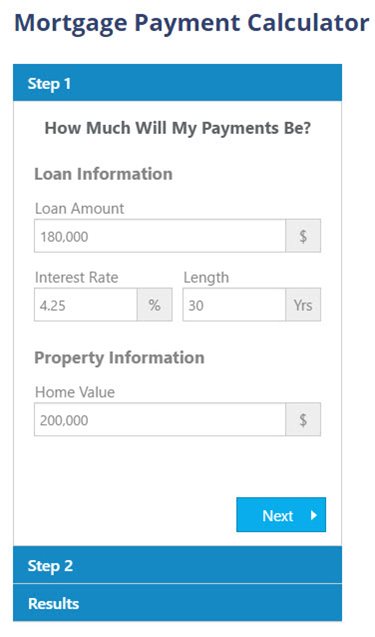

To start using the calculator, know the loan value to home cost ratio for the home you might purchase, for example, are you seeking an 80% loan or a 90% loan? A $200,000-dollar home at an 80% loan value requires a 20% down payment of $40,000, meaning you are seeking a $160,000 mortgage. A 90% loan requires a $20,000 down payment and therefore you’re going to need a $180,000 mortgage. Next, specify the loan and the expected interest rate in the first step.

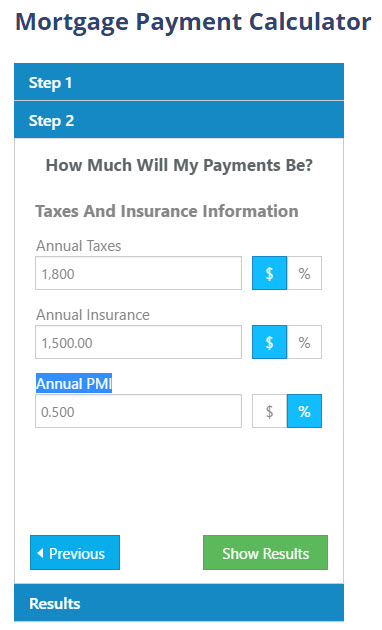

To move to the second step, input the estimated real estate taxes for the house, the annual homeowner insurance expense and private mortgage insurance expense. Your inputs might look like this:

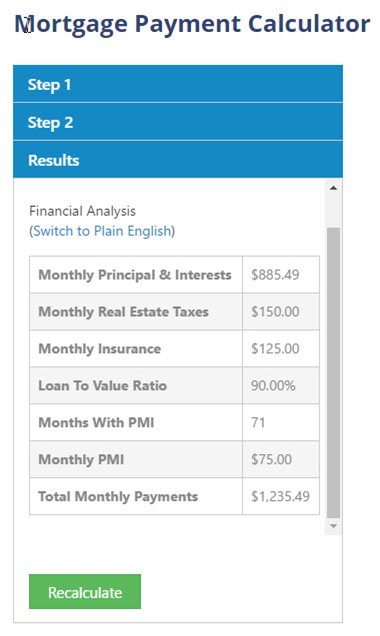

To learn what your payments are with a line by line break-out of expenses, click the show results button.

Getting pre-qualified for a mortgage

Your next step should be getting pre-qualified for a mortgage. Bank of America advises consumers, “Getting prequalified for a mortgage gives you an idea of what your loan program and the amount you could borrow might look like in advance.”

When you’re prequalified your potential lender will ask for some basic information from you. Investopedia notes that you will “supply a bank or lender with your overall financial picture, including your debt, income and assets.” Most lenders may gather information for a pre-qualification over the phone or the internet. There is no commitment by the lender or you to the lender.

Your pre-qualification will give you an idea of the amount of money which you may anticipate borrowing, and then an understanding of the price of the house you can afford.

Once pre-qualified you may choose to go back to the mortgage calculator and use your qualified numbers to further improve your mortgage payment.

Pre-qualified is not pre-approved

If you want to streamline the process of getting a mortgage, you may want to go ahead and get pre-approved. This is a far more complex process which requires a number of financial disclosures, documentation and background information. Realtor.com has a full list of the documents usually required to be pre-approved. You need to have:

- Proof of identity such as your driver’s license or US Passport

- Two years of tax returns and proof of income such as W2s for all buyers

- If self-employed, profit and loss statements for your business

- If you are a renter, you’ll need at least a year’s documentation of timely rental payments

- IRA, Investment and stock statements

- If you have income other than from your employment, you will need proof of that income.

Pre-approval for a mortgage results in your being given a Good Faith Estimate which discloses the expected costs of the mortgage and signals to the seller that you’re a serious buyer.

The US Consumer Affairs office of the Federal Department of Trade has a very detailed mortgage shopping worksheet which you may find of use.

Don’t fear the financial aspects of planning to purchase a home. Provided you get organized, and have kept your financial house in order, you’ll be able to follow the path to a home purchase.

###

Thank you for reading and sharing our articles from The Greater Charleston New Homes Guide. Our business is to know Charleston, SC's new home construction, home builders, neighborhoods, and homes so we may assist you as you take your new construction home journey. Please take the time to explore our site. The Greater Charleston New Homes Guide is considered the best and most reliable ‘local’ resource to new home construction, builders, neighborhoods, and homes throughout the Lowcountry since 2004.

8.17

Tagged as: Home Mortgage Info

Categories: The Guide Tools